Brief About the Company

Alok Industries was established in 1983 & a diversified manufacturer of world-class home textiles, garments, apparel fabrics and polyester yarns, selling directly to manufacturers, exporters, importers, retailers and to some of the world’s top brands.

Alok Industries is fully geared to innovations product developments and have manufacturing facility in 10 different locations in Mumbai, Vapi and Silvassa.

Alok Industries had a turnover of 24153 crores in 2015, and the company was having all the latest technology facilities , plant and machineries and the promotors of Alok Industries seems to be over ambitious as they were kept on expanding the business facilities without looking in to the sustainability of the business & kept on increasing the debt and as a result of it the promotors were failed to repay the debt almost all shares where pledged by them and finally declared as a bankrupt company and filed the bankruptcy in 2017 at NCLT Ahmedabad as per the Insolvency and Bankruptcy Code 2016.

Reliance & JM Financial Asset Management Reconstruction Company jointly came as a successful bidder called as resolution applicants and as per the NCLT order Dtd. 08.03.2019 the Resolution Plan was approved and the same was implemented finally on 22.01.2020 and work as per the resolution plan commenced by the management of Reliance & JMFARC.

In between the implementation of resolution plan after approval by NCLT, resolution applicants made an attempt to take up the matter with NCLAT for delisting of the company however they could not sustained due to the conditions led by in the resolution plan by the resolution professional and strong oppose by the retail share holders.

So as per the approved resolution plan the company is managed by the resolution applicants i.e. Reliance Industries Ltd and the JMFARC trust.

Key Changes in the Company that could attract the investors towards the company

SWOT ANALYSIS

Strengths

- Experience Management Team – Reliance Management is effectively handling the company since implementation of the Approved Resolution Plan.

- Revenue of the Company is increasing QoQ from the past 7 Quarters which is a very good signal.

- Increase in Profits of the company from the past 3 Quarters.

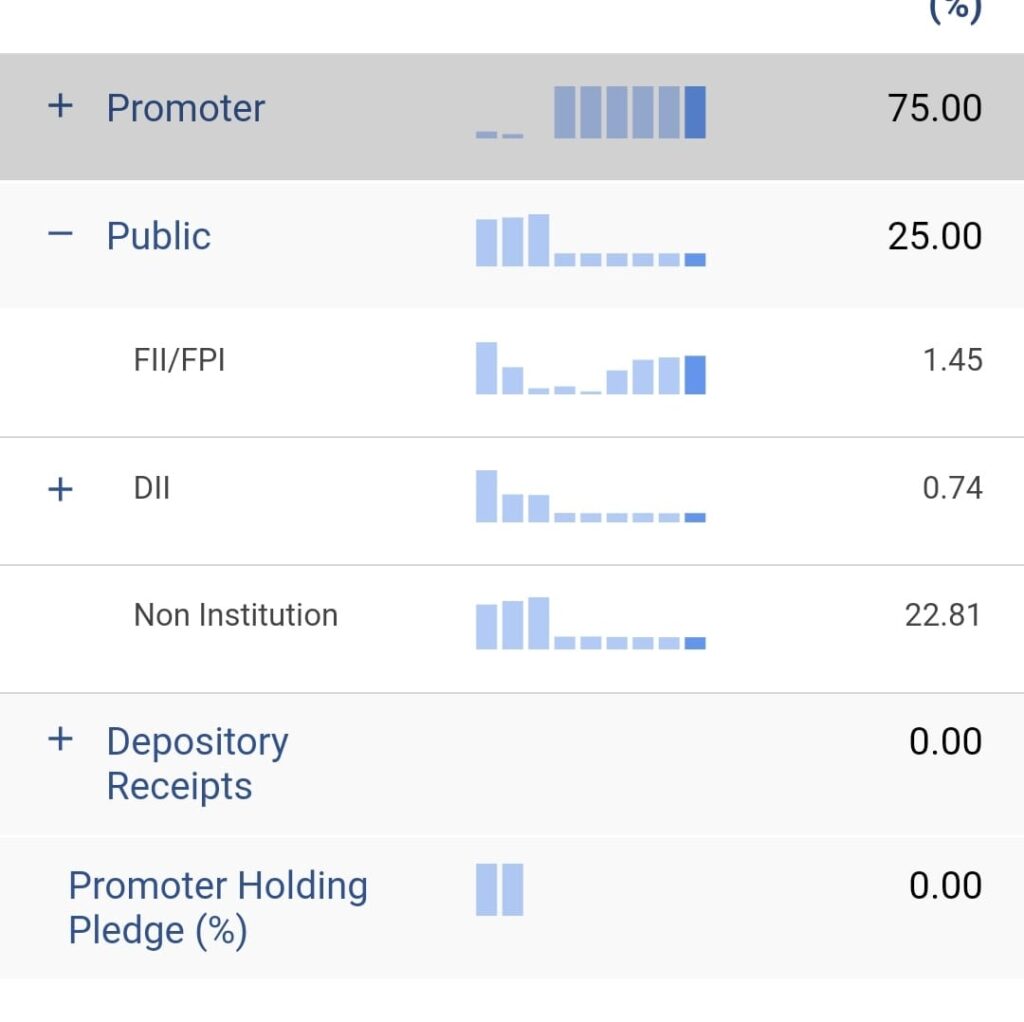

- Promoter Holding is 75%.

- No Pledge by Promoters.

- FII / FPI slowly increasing their holdings.

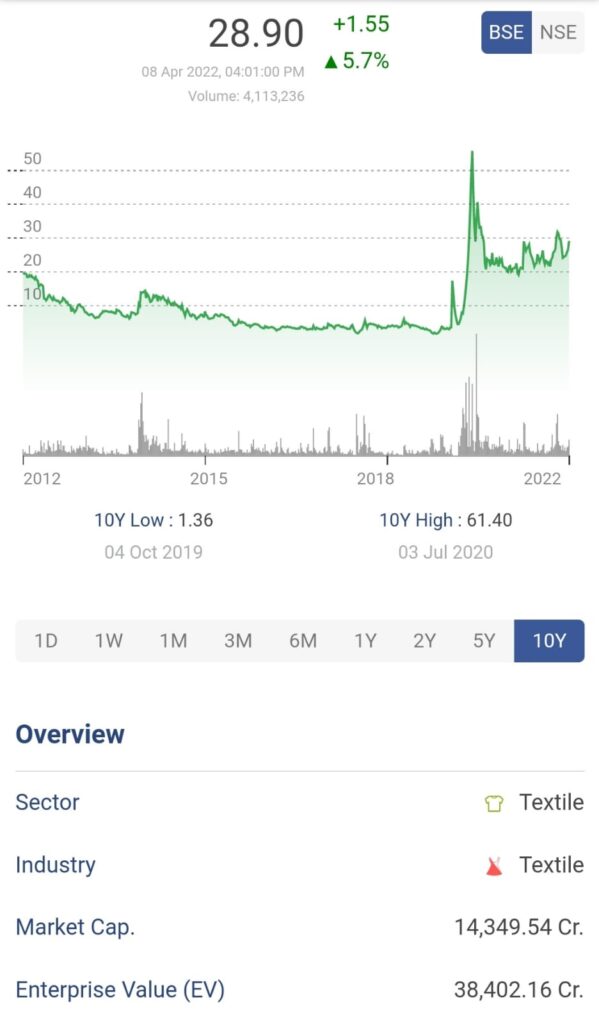

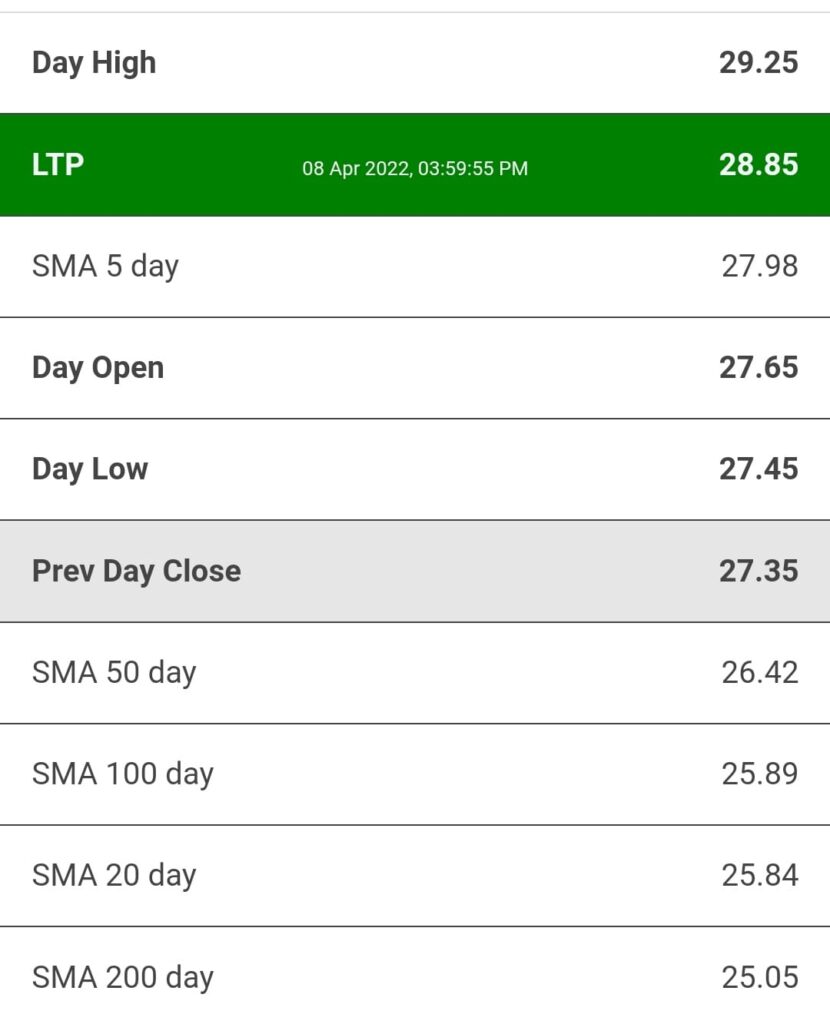

- Strong Price base formation done in the zone of Rs. 20 – Rs. 22.

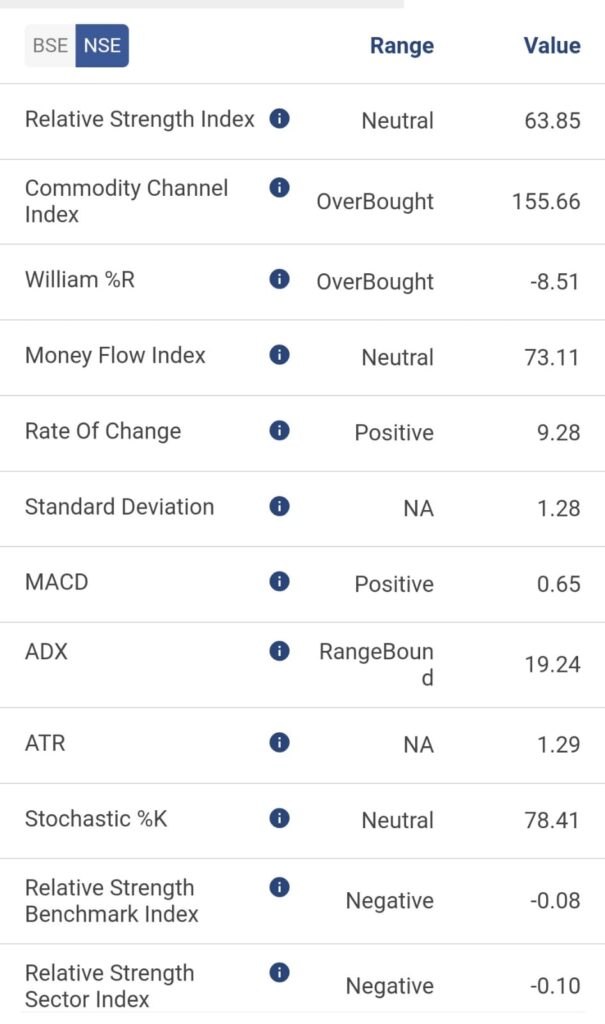

- Strength is seen on the Technical Charts which will be shown in below contents.

Weaknesses

- Capacity utilization of the company is still lesser & still the utilization is below 50%.

- New Management still not came forward openly with the commentary on the growth plans of the company.

- Net Cash Flow is Negative.

Opportunities

QoQ Results seen growth and results in positive shift in the share price of the company.

Going forward the company is expect to deliver the better performance in terms of sales and net profits of the company.

Strong Business Opportunities in the domestic and international markets.

Company is having Global presence and due to huge textile demands from US the company’s exports are increasing and further have high potential.

An Edge over the Quality of the Products and established brand & Reliance Retail – has strong business network and shift in the vision of the Reliance in Retail business.

Threats

Increase in Cost – Direct and Indirect cost seems higher.

Less Utilization of Assets – Cost Effectiveness.

Strong Competitions from the peer group companies.

No new product developments.

Technical Chart

Stock is Moving in a Upward Sloping Channel with the support at 22.50 & Resistance at 33.50.

Price Momentum indicating the positive shifts in the price and the stock probably could touch first at 33.40 levels and then can take a further direction.

RSI showing the strength in turn looks bullish.

Short, Medium and Long Term Moving Averages showing Bullish momentum.

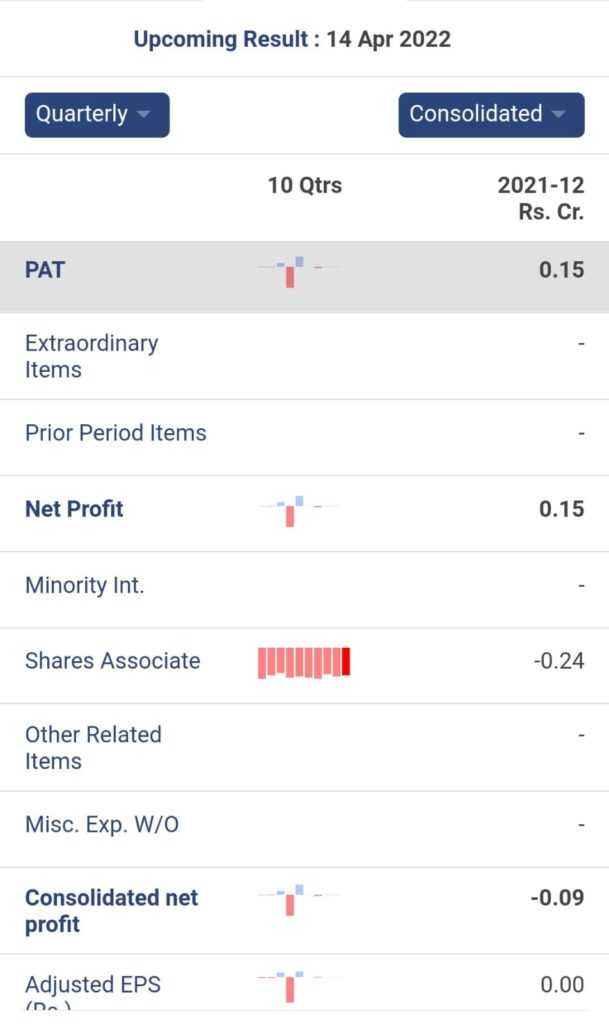

Q4 Results Expectations

- Q4 Revenue in the range of 2500 to 2700 crores i.e. 18 to 30 % increase QoQ approx.

- Operating Profits / EBITDA – Approx. 360 to 400 crores. An increase of 12- 15 % expected.

- Company is expected to declare net profits in the range of 45 to 80 crores in Q4.

- Annual Revenue – 7700 to 8000 crores.

Forward Expectations in FY 2023

QoQ increase of 12 to 15% in Revenue in turn annual revenue is expected in the range of 12000 to 15000 crores.

Company Expected to be net profitable in FY 23.

PAT is estimated at 1500 crores in FY 23.

EPS expectations – Minimum Rs. 5 / -.

Present Market Cap of the Company Stands at 14325 crores at CMP – 28.80.

Future Market Cap at the End of FY 23 is expected in the range of 40000 crores to 50000 crores in turn the share price is expected to be at minimum of above Rs. 100 /-.

Disclaimer :-

All contents posted here are for Educational Purpose Only and do not treat it as a recommendations to buy or sell. Do your own analysis / consult your financial advisor before taking any investment decision.

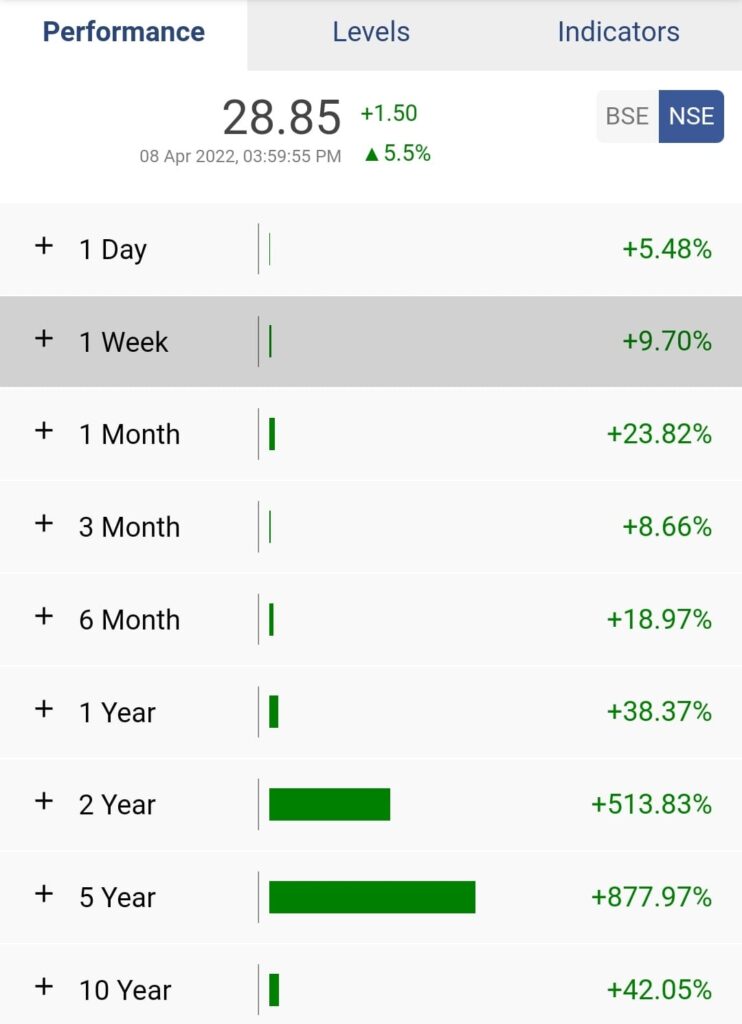

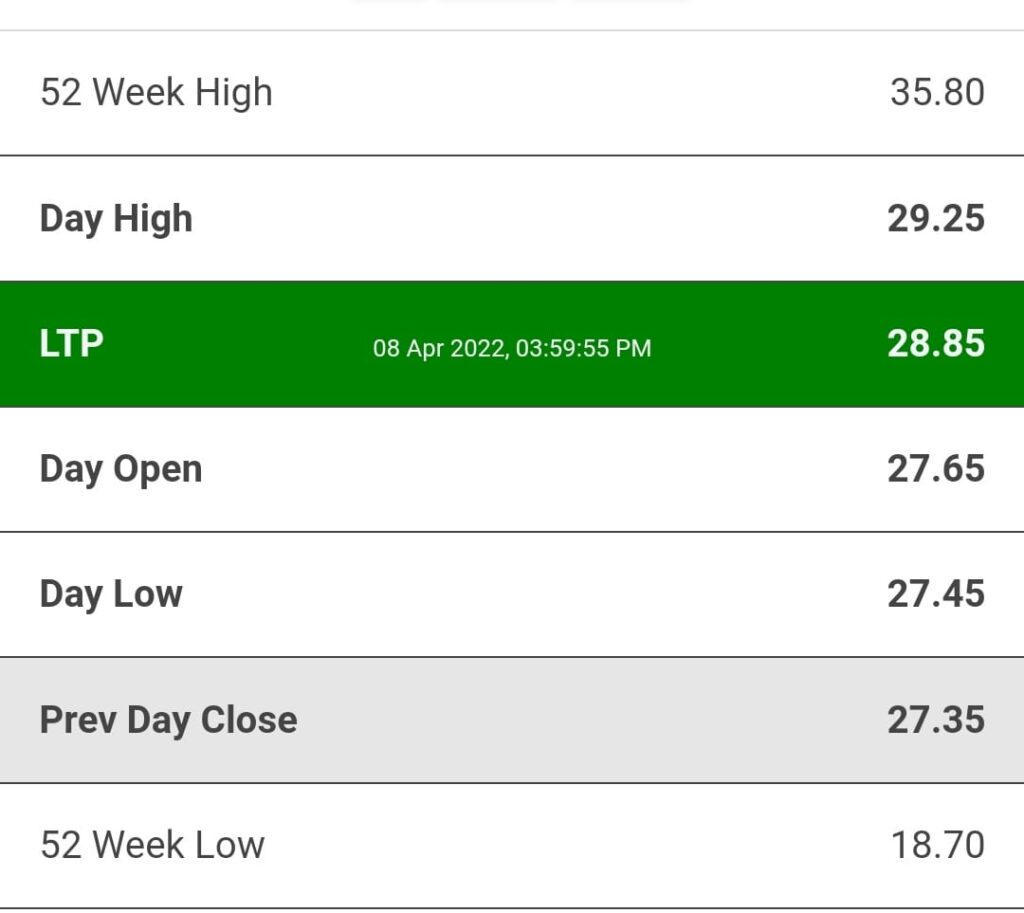

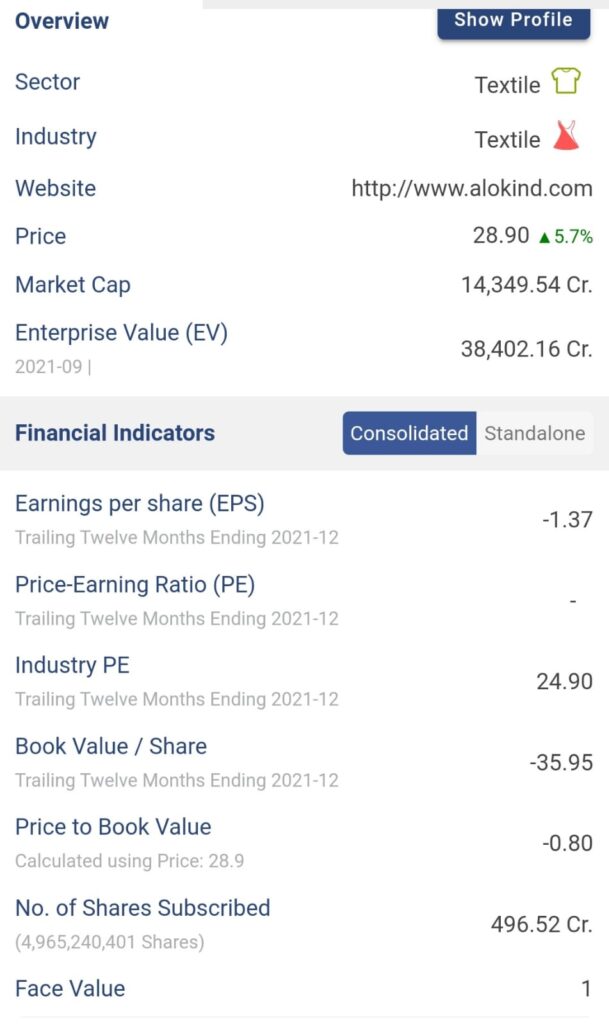

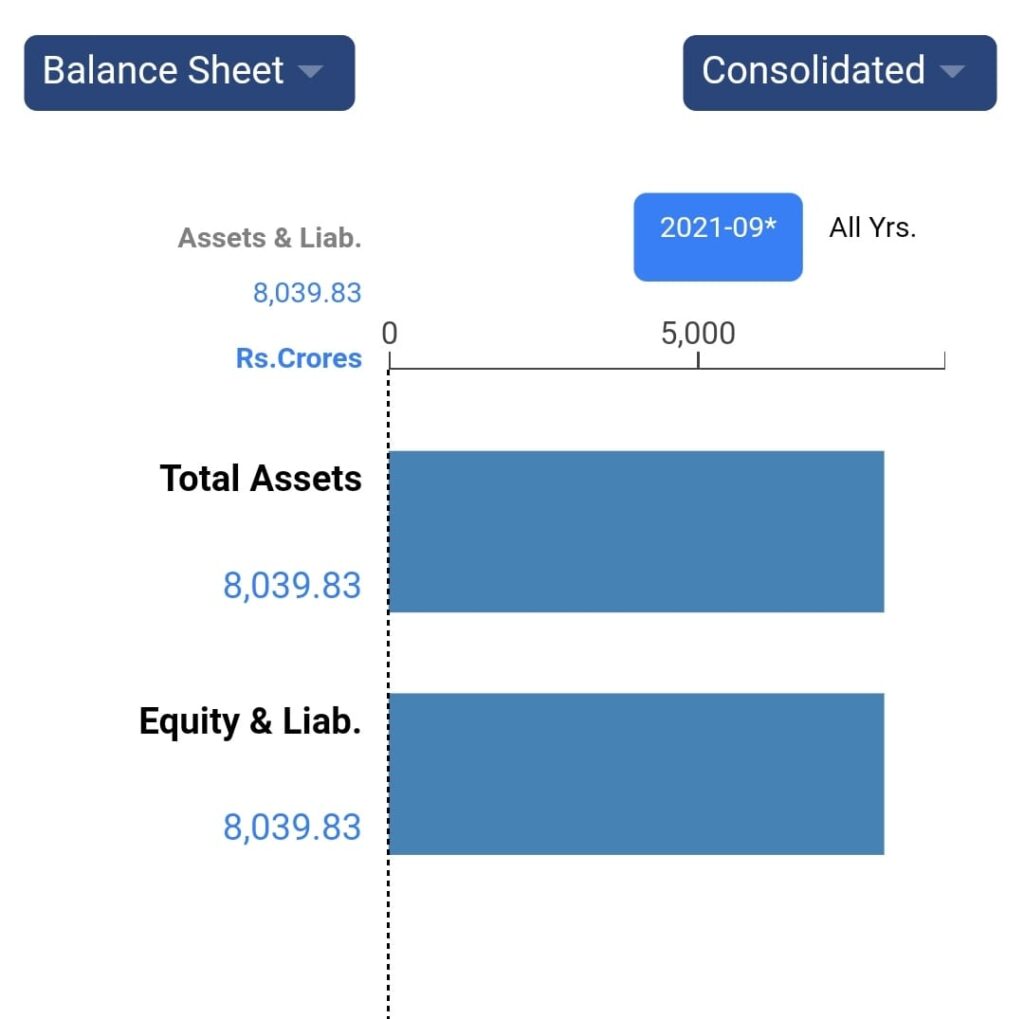

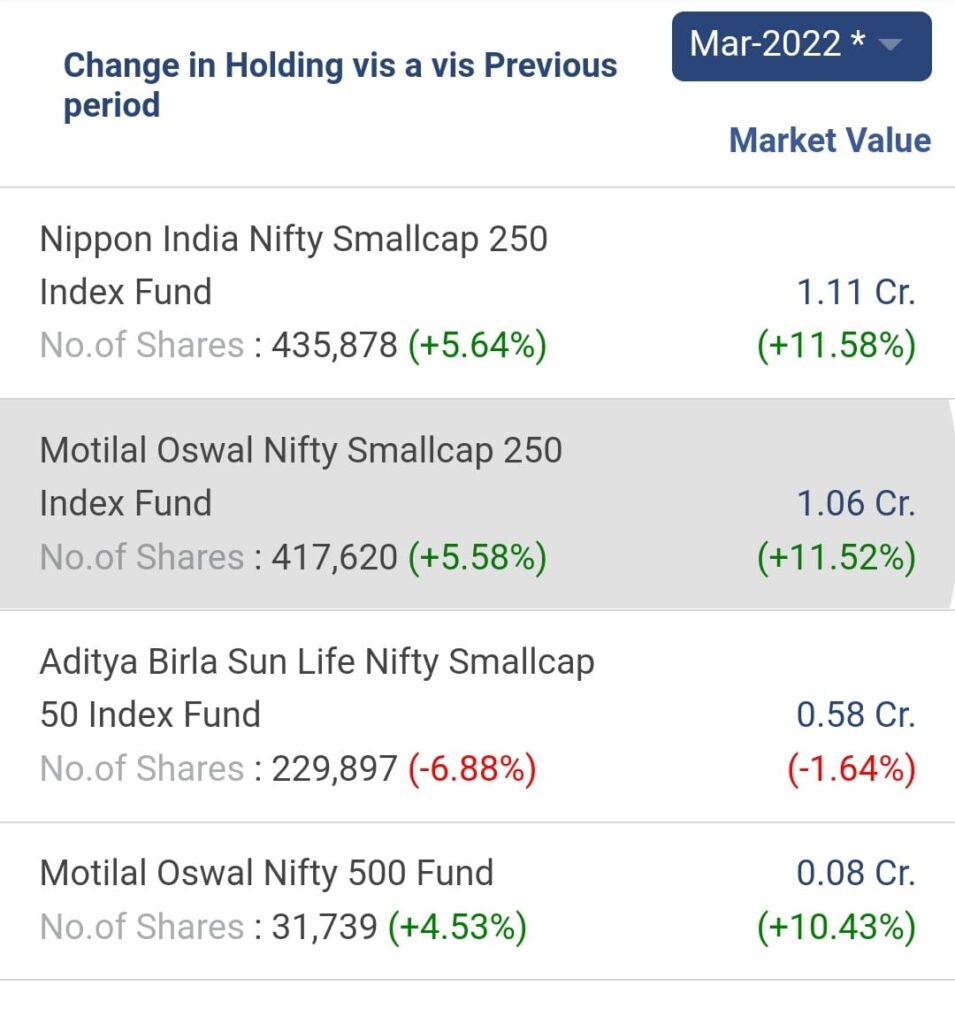

Below Snaps of Alok Industries are updated from StockEdge for kind reference to all of you and if required can be viewed on StockEdge is a good App for all investors needs.