Options Trading – A Complete Guide for Beginners – Understanding the Options trading and why to choose Options trading?

Introduction

The contents posted here are basically focused for Options Trading in India and the concepts are same as it can be implemented anywhere, so let’s get started why people in India prefer trading in India so my simple answer is the for Options Trading it requires lesser capital, this is how the though process in Indian Traders goes on and in the recent change in the nifty and Banknifty options trading weekly expiry really changed the people thoughts as on expiry day you can see the volume of options trading as it looks like a gambling only but those who really understand the options and implement the same in conceptual and in practical does really going to help the traders. As mentioned our theme of SSV Education is focused on the retail traders and how we can participate in helping the peoples so that they can earn money and become independent traders and investors. NSE is the largest platform of Options trading in the world, so Do you think that’s the reason for Choosing Options trading? You will be able to find the answer in this series of Options Trading and concept and you will be able to select the correct trading strategies for implementing the same in your trading life or will be useful for modification in your strategies.

Why Option trading is getting popular day by day is basically due to its simplicity and lower risk profile. Do you agree or Not? No its not true and simple however if you follow the Options in the right path you will be able to make living out of it.

Most of the traders thought is that it requires less money and it can give a regular income as options required very little knowledge to start with so first of all, I will like to mention here that Options Buyers wining rate is only 5% and Options Sellers win rate is 95% as the 95% Options expires worthless. From this you can judge which is better options for choosing you. However it does not mean that Options Buyers didn’t earn so you have to follow and understand in and out of the Options. The more simple you keep the more you will be able to fetch the returns and for that the trading discipline and money management and traders psychology is very much important aspect.

One thing you must understand that the most important advantage of option trading is that Options trader can make profits irrespective of the market direction and market conditions. Only thing is that the Option Trader has to select the right trading strategy depending upon the type of stock of the index and the direction of markets.

Now lets us discuss the advantages Of Options Trading One by One

- Cost Efficiency: Options have great leveraging power, Options trading allows you to trade with a small amount to take control over the larger amount of the asset. (Underlying asset). For example, if a trader wish to own 25000 shares of XYZ company trading at Rs. 100, so he requires Rs. 2500000/-, but he didn’t have that much amount of money so he can choose to own the stock by taking position through options. Yes he can take a position by using options, but obviously it is not so simple and the options trader has to select the correct strike call options. So it is possible through stock option and it is called stock replacement strategy and is cost effective.

- Flexibility: Options trading offers more investment alternatives and Option trading is a very flexible investment tool. In case of trading with future or underlying asset, one can trade under two situations i.e. underlying asset price is in rising mode or the underlying asset price is in declining mode .One has nothing to do when market is stagnant. But options allows trading and making profit in below mentioned conditions

- Underlying asset price is moving. i.e. Higher /Lower

- Underlying asset price is moving too slowly

- Active Market Direction / stock price movement is not clear i.e. trading in a range

- Volatile Conditions i.e. Increase or Decrease in volatility.

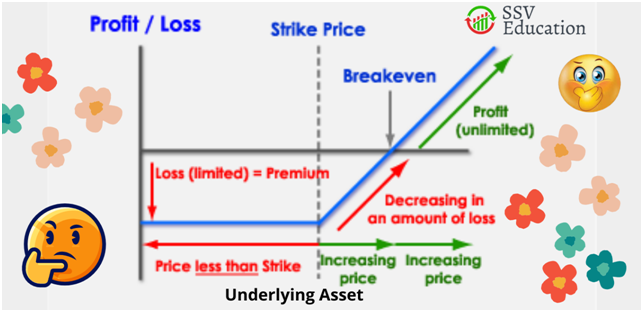

- Higher Profit Potential with limited Risk: The maximum loss is limited when someone buys an option but the possible profit amount is unlimited but this situation may also change depending on the option strategy.

From the above diagram you can clearly understand limited risk while owning a call option and this risk amount is limited to the premium paid for buying the option where as owning same amount of underlying asset has unlimited loss.

The factors which can affect the option price are underlying asset price, time and volatility. Option strategies can be created or adjusted by manipulating these parameters as per one’s risk-reward tolerance ratio.

Portfolio protection is also possible by creating hedge with option to fight with adverse situation.

Understanding Options, What is Options?

An option is a contract between two parties giving the buyer the right, but not the obligation, either to buy or to sell an underlying asset at a set price, on or before a predetermined date. In other words you can say option is the right either to buy or to sell a specified amount of a particular underlying asset, at a pre-determined price by pre-determined expiration time frame.

Option is known as derivative because its value is derived from an underlying asset and its price fluctuates as the price of the underlying asset rises or declines.

There are two types of options i.e. Call Option and Put Option. Now lets understand the Call Option and Put Option One by One

Call Option: A call option is the right but not the obligation to buy a fixed amount of share at fixed price on or before the expiry period. If the trader is expecting an upside movement of the stock or market then he should buy call Option of that stock or index call option of the market (e.g. Nifty & Bank Nifty). If a trader is having bullish view on the banking stocks then he can think of buying Banknifty call options and vice-versa. Seller of a call Option is have an obligation to buy the underlying asset if not squared off.

Put option: A put option is the right but not the obligation to sell a fixed amount of shares at fixed price on or before the expiry period. If the trader has a bearish view on market or a particular stock then he should buy put option of the market or put option of that particular stock.

Important terminologies used in Options trading

Underlying Asset: Each option is based on an asset; this is known as underlying asset. This asset may be shares of a stock or value of an index.

Strike Price: The strike price (or exercise price) is the predetermined price at which the underlying asset may be bought by the call holder or sold by the put holder.

Expiration Date: This is the date on which an option expires.The trader may close their positions before or on the expiry day. Normally the monthly option expires in the last Thursday of every month in India. Nifty and Bank Nifty Weekly Options expires every Thursday of the week and in case of holiday on previous trading day.

Option Premium: The price paid for buying the option is known as option premium or simply option price. The buyer pays the option premium to own the option and the seller of the option receives that premium. The premium depends on different parameters.

This premium can be divided into two parts; intrinsic value and time value & we will explain the same with examples at the later part.

Parameters affecting option premium

A trader should have clear knowledge on the parameters which affect the option pricing. The option price generally depends on the underlying asset, volatility, time left for expiry and interest rates. All of these factors will be discussed in details in option Greeks topic.

In-The-Money Options (ITM Options): A call option will be known as in-the-money option (ITM) when the strike price is lower than the underlying asset price. On the other hand, a put option will be in-the-money option when strike price is higher than the underlying asset price.

At-The-Money Options (ATM Options): When underlying asset price is equal to strike price of the option, the option is known as At-The-Money option.

Out-of-The-Money Options (OTM Options): A call option will be known as out-of-the-money option when the strike price is higher than the underlying asset price. On the other hand, a put option will be known as out-of-the-money option when strike price is lower than the underlying asset price.

Now Let us understand the above mentioned terms in the Options Chain Data

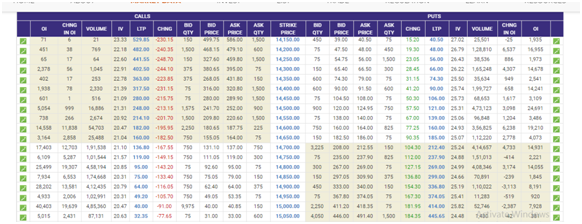

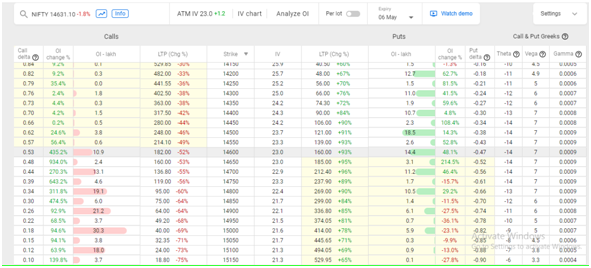

Now just refer the below Options Chain data for Nifty, which is obtained from NSE India’s website and you can see that Nifty is closed at 14631 and understand the different strike price’s at the middle of the options chain data

Here expiry date is 6th May 2021 (Weekly Expiry Date of Nifty Options). It indicates that these listed options should be traded on or before 6th May 2021.

The call options are listed on left hand side and put options are listed on right hand side.

Strike Price of the options is listed just middle of the two types of options. As the underlying index (nifty) price is 14631, so the call and put option of strike price 14650 (+/-50) are at-the-money (ATM) option. The call and put options of strike prices below 14650 are in-the-money (ITM) call option and out-of-the-money (OTM) put options respectively.

The call and put options above 14650 are out-of-the-money (OTM) call options and in-the-money (ITM) put options respectively.

In the above table, option premium or option price is denoting by the columns “LTP”(Last Traded Price) ,Bid Price and Ask Price.

Bid Price is the price at which buyers in the market are interested to buy that particular option so that you can sell your option at that price. Ask price is just opposite to that.

“The price of Nifty call option of strike price 14600 of 6th May 2021 weekly expiry is Rs. 182 as on 30th April 2021 when the price of Nifty is 14650.Lot size of Nifty is 75 Qty.”

The above statement is indicating the below mentioned facts:-

- The Nifty call option of strike price 14600 is in-the-money (ITM) option as strike price is lower than the underlying asset price.

- The buyer of this option trader has the right but not the obligation to buy 75 qty of nifty at Rs.14600 (strike price) within the pre-mentioned time frame i.e. coming Thursday 6th May 2021. To buy this right, Option buyer has to pay Rs.182 X75 = 13650/- (option premium).

Hence, Option Buyer should exercise the option when it will be profitable i.e.when the underlying asset price will be above Rs.(14600 + 182)= 14782.

- Intrinsic value is the in-the-value portion of an option premium i.e. the difference between the underlying asset price and the strike price when the option is in-the-money option.

Here intrinsic value of the call option of strike price 14600 is (underlying index price i.e. 14650 – strike price i.e. 14600)=Rs.50/-.

But the option premium is Rs.182. Hence the difference between the option premium and intrinsic value is the time value of the option premium.

Most important factors affecting option Price other than asset price

Volatility: Volatility refers to the price fluctuation of underlying asset. This volatility can be of two types: Historical volatility and Implied volatility.

Normally option premium increases as volatility increases and vice versa.

Historical Volatility: Historical volatility is the historical price fluctuation of the underlying asset in percentage terms. Normally it is calculated as standard deviation of daily fluctuation of historical closing prices. Calculation of historical volatility will be discussed subsequent sections.

Implied Volatility: Implied Volatility (IV) is one of the most important deciding factors of option price. We found Historical Volatility is the annualized standard deviation of the past price movement of a stock or index. But Implied Volatility is the volatility that matches with the current option price and indicates current and future perception of the market risk. In one sentence, implied volatility is the volatility which market implies about the stock’s volatility in the future.

It is important because option price increases if implied volatility increases keeping other parameters remain constant.

You can get implied volatility of option prices in NSE websites or any other financial websites or software’s where option chains are available.

Days or Time to expiration: The time remaining in days to the expiry period is an important factor to determine option price. The value of option decreases as the time to expiration gets closer. The more time remaining until expiration, the more time value of the option contract has.

Option Greeks

Option Greeks are quite interesting. These are collection of statistical values named after Greek letters. If you want to gets success in option trading and if you wish to take this profession as your full time earning option then you should understand each and every Option Greek.

The Option Greeks can be very useful to help you to predict future option price because they effectively measure the sensitivity of the price compared to some of the factors that affect price. In particular, these factors are underlying share price, decay in time, interest rate and the volatility.

If you know how option price changes with respect to these factors, youareinabetterpositiontoknowhowtransactionswilltakeplaceinfuture.The Greeks will give you an indication of how the price of an option willmove compared to the way the underlying share price movements and theyalsohelpyoutodeterminetheamountoftimeanoptionlosesondailybasis.

The Greeks are also risk management tools because they can be used to determine the risk of a particular position and find out how to mitigate that risk.

First time, these terms may look cumbersome or may feel difficult to understand but once you will understand their role in option trading; the work will be easier for you. Of course, you can learn how to calculate the Greeks, but it is a complex and lengthy process. There are many softwares available in the market which can be used for this and most of the best online brokers offer automatic values for the Greeks in their display box of option chain.

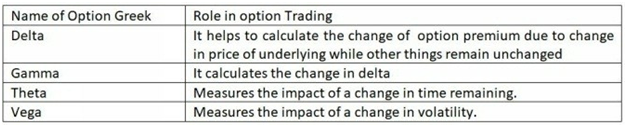

There are five types of option Greeks Delta, Gamma, Theta, Vega and Rho

Delta :

Option Delta is the most important Greek to understand because it indicates sensitivity of option prices in relation to the price of underlying. In simple terms, it’ll tell you changes in option price due to change in 1 unit of underlying price.

An option with high delta will move in price significantly in proportion to the price movements of the underlying security, while one with low delta will move less often.

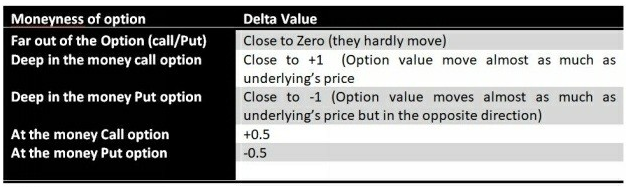

The delta value of an option is usually expressed as -1 to 1. Normally delta of a call option is expressed from 0 to 1 and delta of a put option is expressed as -1 to 0.

The value depends mainly on the moneyness of a particular option i.e. whether the option is in-the-money or at-the-money or out-of-the-money.

Delta of any option can tell you the type of the option. Please follow the table to know in details:-

Normally, delta of a call option is positive. It means when we buy a call its delta value will be positive and when we buy a put its delta value will be negative. But this positive / negative sign will be opposite in case of selling.

Table showing positive / negative sign of call and put option

How to calculate option price with respect to underlying’s price change depending on delta value

Suppose a trader holds a call option which is slightly in-the-money with a delta of 0.6 and market price of 10. This call option gives you the right to buy 100 shares of company XYZ for Rs.150. Currently the company XYZ is trading at Rs.160.What will happen if the stock price increases to Rs.170?

Here the strike price of the given call option is Rs.150; market price of call option (150 strike price) will increase by Rs.0.6 For an increase of stock price by Rs.1.

Therefore, if stock price increases by Rs.10 then the option price will increase by 10*0.6=6

i.e. the call option price will be Approx.(10+6)=16 if the stock price increases to Rs.170.

How to calculate the delta of an option strategy /Portfolio

You can easily calculate the total delta of an option strategy or a portfolio by summing up deltas of all individual options.

For Example,

Suppose a trader have made an option strategy with the following option:-

1 ITM long call with delta 0.55

1 ITM long put with delta -0.6

1 OTM short call with a delta 0.3

1 OTM short put with a delta -0.4

The total delta of this position is: 0.55+ (-0.6)-0.3+0.4 =0.05

It indicates that the market value of your option strategy or portfolio will increase by 0.05 unit for 1 unit move of the underlying’s market price.

Note: Normally sign of delta of a put option is negative. Delta sign will also be negative when we short any call option. Whereas the sign will be positive for a shorting put option.

Importance of Delta Neutral Option Strategies

As you know, trading in derivative is somehow speculative because most of the action depends on trader’s view on the stock or the market. This market outlook of the trader may be faulty and may end in huge losses. In this case, delta neutral strategy helps a lot. A delta-neutral strategy is a weapon of a trader which he can use to earn profit without forecasting the direction of the market.

The term “Delta Neutral” refers to any strategy where the sum of delta values of all the options is equal to zero. For an example, if you buy 2 call Options, each having a delta of 0.60 and you buy 4 put options also, each having a delta of -0.30 then you have the following:

Summing up the delta value = (2×0.60) + (4x-0.30) =1.2-1.2=0 Hence, position delta (total delta) is zero here this is known as Delta Neutral.

In practical, this type of option strategy will not get affected due to small movement in stock price or market but delta neutral position will not necessarily remain neutral if price of the underlying security moves to anyside at great degree. Because, delta value of the option will change a lot if stock price moves in any one direction significantly.

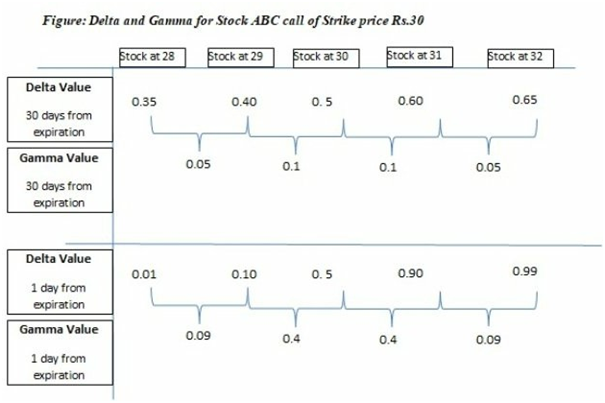

Gamma

Gamma is the rate of change of an option’s delta i.e. gamma denotes how an option delta value change with 1 unit movement in underlying’s market price. You need to reduce the gamma if you want to make a delta hedge option strategy for a wider price range.

Mathematically, delta is the first derivative of the option market price and gamma is the second derivative of the option price. When the option is deep in-the-money or out-of-the-money then the gamma value is small but when the option is near or at-the-money, gamma value is the largest.

All long option have positive gamma and short option have negative gamma. Hence, the trader can calculate the positional gamma for a particular option strategy by summing up gamma of all individual options.

In the above figure, the strike price of the stock is Rs.30. So, when the stock price moves up or down from Rs.30, the option moves in or out-of-the-money. As you can see that the price of the option for at-the-money call changes more significantly than the other two types call i.e. in-the-money or out-of-the-money call.

Also it is clear from the gamma value that the rate of change in price is higher in case of near term option than the longer term option.

What to see as a trader?

As an option buyer, your primary aim will be for higher gamma value.Your option Delta will move towards the value 1 more rapidly as the call price will be move towards in-the-money. Hence, you will gain more if your prediction is correct.

On the other hand, if your prediction goes wrong then this higher gamma value may bring big losses.

So, always try to keep balance between all Greeks.

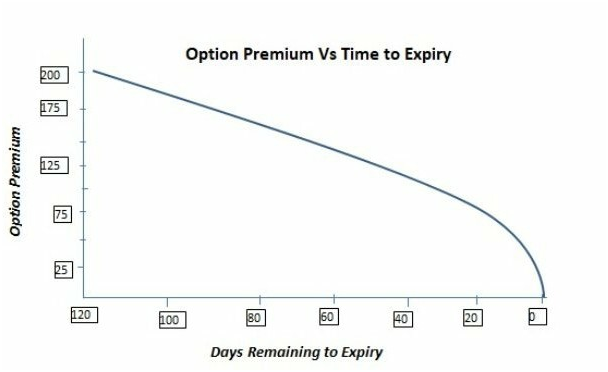

Theta

Theta, the third option Greek, indicates the decaying of option value overtime. It is the ‘silent-killer’ for option buyer as it takes away all the option time value as the expiration comes near and theta value of option becomes zero at expiry.

As you know the Option Value = Intrinsic Value+ Time Value

Here this “Time value” depends on the value of theta. If the theta value is high for any option then its time value will decrease fast.

Theta values are always negative for option buyers and always positive for the option writers or sellers.

As you can observe in the graph, effect of theta is low on the option premium when expiry is far and the effect of theta becomes high on option premium as expiry comes near.

Being an option trader, you can take advantage of theta by opening credit spread position or by simply selling options. As time passes on, if the stock price remains same or does not change significantly or simply stays out-of-the-money then option value will decrease a lot and you will be able to keep the selling option premium with you.

On the other hand, if you are an option buyer then try to close down your

Position within few days as theta can takes back your profit as the option reaches near to expiry.

Vega

Vega measures the change in option premium due to one unit change in implied volatility. Implied volatility indicates the expected volatility of the underlying asset over the life span of the option and not the historical volatility of the underlying asset.

The above table is the nifty options chain with 6th May expiry with their Greek values. If you observe the values carefully you will find that the Vega value is higher for at-the-money options compare to the in-the-money or out-of-the-money options.

Normally option price increases if implied volatility increases. Long options have positive Vega and short options have negative Vega. Like theother Option Greeks, you can calculate the positional Vega of a strategy by summing up all the individual Vega value.

More Details on Options Coming Soon in the our next Topics so stay tune and do share feedback with us.